Audit & Assurance exam has a regular question on the Audit Risk & the Response. The examiner may ask you to describe up to 8 Audit Risks along with the Auditor’s response. That means 16 marks in total. It may be less for instance 5 or 6 risks, depending on the marks. A good thing

Ethics Issue Threat Safeguard Financial interests SELF-INTEREST THREAT Disposing of the interest Removing the individual from the team if required Close business relationships SELF-INTEREST THREAT & INTIMIDATION THREAT Terminate the business relationship Refuse the assurance engagement. Employment with an audit client

Latest ACCA AAA Pocket Notes 2020 You can download the Latest ACCA AAA Pocket Notes 2020 for your upcoming exams and we would like to recommend that you must go through them. Dear Students, you can as you know that only the text and practice kit are not enough to pass your exam in the first

ACCA Becker Revision Mocks and Solutions For F5 to P7 Performance Management for June 2017 Attempt, you can download the ACCA Becker Revision Mocks in PDF format here free. To download these mocks and their solution please click the download link provided below. June 2017 F5 Exam

ACCA P7 AAA Important Technical Articles At the end of this post, you will find the download link to ACCA P7 AAA Important Technical Articles in the pdf format. These, ACCA P7 Technical Articles will help you to prepare for your upcoming exams. This material is helping many students in their ACCA Exams and passes

Very Important International Accounting Standards Notes You can download the Int. Accounting Standards Notes your upcoming exams and we would like to recommend that you must go through them. Dear Students you can as you know that only the text and practice kit are not enough to pass your exam in the first attempt. You

Latest ACCA AAA Prepare to Pass for September 2019 You can download the Latest ACCA AAA Prepare to Pass for September 2019 for your upcoming exams and we would like to recommend that you must go through them. Dear Students you can as you know that only the text and practice kit are not enough

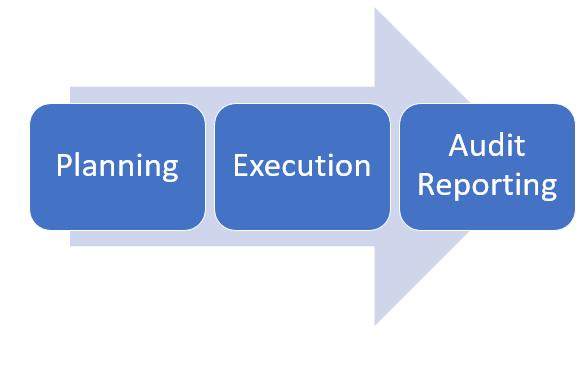

Very Important Topics of AAA by Sir Rashid Hussain Advanced Audit & Assurance (P7) – Important topics for September 2019 Question # 1 Business Risks Risks of Material Misstatements along with analytical procedures Audit Procedures Ethical Issues Knowledge Based Part Important Standards you should know for Q1: IAS 2,16,21,23,33,36 IFRS 2,8,15 & 16 Important Procedures

Latest ACCA Study Material At the end of this post, you will find the download links Latest ACCA Study Material till 2020 Short, simple, exam focused revision notes, essential support for anyone who wants to acquire knowledge of the paper and also learn how to pass the paper.A must go through resource before the exam.

Latest ACCA Study Material Download 2019 – 2020 is available for download on one click, you can download ACCA KAPLAN Study Material in PDF format at one place. Latest ACCA Study Material Download 2019 – 2020 will help you to prepare for your exams and get high marks. You can cover your syllabus within a

ACCA Optional Level March 2019 Exam Tips Advanced Financial Management (AFM) March 2019 Exam Tips From September 2018 every exam will have questions which have a focus on section B of the syllabus (advanced investment appraisal) and section E (treasury and advanced risk management techniques). These syllabus areas are therefore high priority areas for your revision.

ACCA P7 AAA Exam Practice Tips At the end of this post, you will find the download link to ACCA P7 AAA Exam Practice Tips. These, Latest ACCA P7 AAA Exam Practice Tips will help you to prepare for your upcoming exams of ACCA AAA. Students must know that these materials are there to help them